Many Families Would Struggle to Pay a Typical Health Insurance Deductible, New Analysis Finds

Fewer than Two Thirds of Moderate-Income Households and One Third of Low-Income Households Have Sufficient Financial Resources to Cover Mid-Range Deductibles

Many families – especially those with low to moderate incomes -- don’t have sufficient savings in the form of liquid financial assets, such as bank balances, CDs and stocks, to cover a mid- to higher-range deductible in a private health insurance plan, a new Kaiser Family Foundation analysis finds.

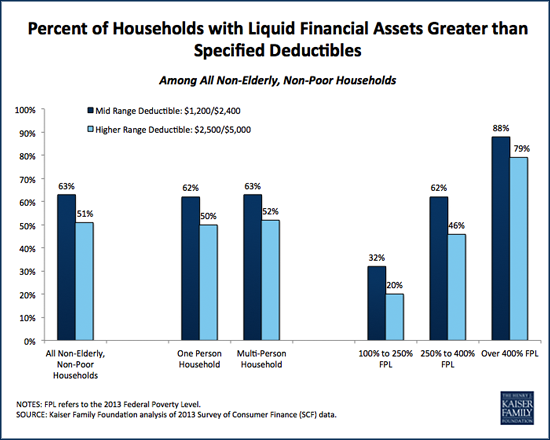

Consumer Assets and Patient Cost Sharing finds that less than two-thirds (63%) of non-elderly households with incomes above the federal poverty level have sufficient liquid financial assets to cover a mid-range annual deductible of $1,200 for an individual or $2,400 for a family. By comparison, the average general annual deductible for single coverage among workers enrolled in an employer-based health plan was $1,217 in 2014.

About half (51%) of households have enough liquid assets to cover a higher-range annual deductible of $2,500 for an individual or $5,000 for a family. In 2015 plans offered through Healthcare.gov, the average combined medical and drug deductible for single coverage in a silver plan was $2,556.

In moderate-income households, 62 percent have sufficient liquid financial assets to cover a mid-range deductible, compared to 38 percent that do not. Less than half (46%) have enough to cover a higher-range deductible. These moderate-income households have incomes between 250 and 400 percent of the federal poverty level ($29,425 and $47,080 for an individual this year). Households at this income level are not eligible for government cost-sharing subsidies that can significantly reduce deductibles and other out-of-pocket expenses for plans purchased in the Affordable Care Act’s insurance marketplaces.

Among lower-income households, a third (32%) have sufficient liquid financial assets to cover a $1,200 deductible for an individual or a $2,400 deductible for a family, and one in five (20%) have enough to cover an annual deductible of $2,500 for an individual or $5,000 for a family. This group has income between 100 and 250 percent of the poverty level ($11,770 and $29,425 for an individual). These households may be eligible for cost-sharing subsidies through ACA marketplaces if they are not offered affordable employer coverage.

Among all households without enough liquid financial assets to meet the mid-range deductible amount, the analysis finds that less than half (47%) could obtain $3,000 from friends or family to help them with an emergency. The analysis also compares household assets to typical out-of-pocket limits for health plans and examines assets versus out-of-pocket insurance requirements for households in which someone is uninsured.

The new study uses information from the Federal Reserve Board’s 2013 Survey of Consumer Finance to compare the liquid financial assets of households with a range of incomes to cost-sharing amounts that are representative of insurance plans offered by employers or available in the individual market, including in the ACA marketplaces. Information about insurance plan design was drawn from previously-released Foundation resources. The analysis makes the conservative assumption that a household can devote all of its liquid financial assets to paying for health needs.

Filling the need for trusted information on national health issues, the Kaiser Family Foundation is a nonprofit organization based in Menlo Park, California.