How might insurers' health fare under GOP plan?

How would insurers fare under the GOP's proposal to replace Obamacare?

It depends.

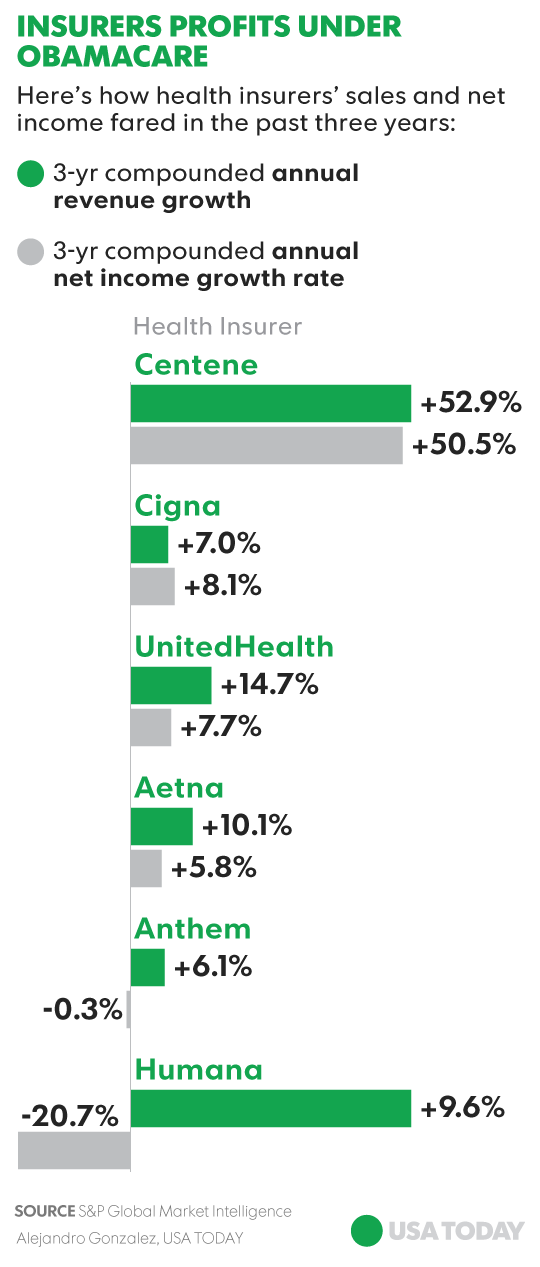

A review of profit results for the six health insurers in the Standard & Poor’s 500 stock index since the start of 2014 — the year the Affordable Care Act rule went into effect that mandated that people who can afford coverage must get it or pay a fine — shows mixed results. The combined net income of Aetna, Anthem, Centene, Cigna, Humana and UnitedHealth grew at an annual compounded rate of 4.7% in the three years ended Dec. 31, 2016, data from S&P Global Market Intelligence show. Overall, the 60 health-care stocks in the S&P 500 grew at an annualized rate of more than 16%.

The results are heavily skewed by Centene, the biggest Medcaid-focused insurer, with roughly 1 million insured through the program, which provides medical benefits for low-income people. During that same three-year period, Centene's net income jumped at an annualized rate of 50.5%, compared to a nearly 21% drop in net income for Humana. By that measure, Cigna's profit rose 8.1%, UnitedHealth's rose 7.6% and Aetna's grew nearly 6%. Centene also benefited from last year’s nearly $7 billion merger with rival HealthNet, which more than doubled the number of people the combined company covers.

How the insurers fare under a new plan will hinge on its final details, insurers’ exposure to the ACA exchanges where people who don’t have coverage can sign up for a plan, and how much of their total revenue is tied to businesses related to Medicaid recipients.

“Centene benefited from the Medicaid expansion,” says Michael Newshel, a managed care analyst at Evercore ISI. “Humana just saw a lot bigger losses in the health care exchanges. Their pricing was a lot farther off and they attracted a worse mix of patients.”

Most of the other major insurers lost money from their participation in the ACA insurance exchanges, due to poor pricing, too few healthy new customers and too many sicker ones, which pushed up costs.

“The idea was the insurers would get all this new business under ACA,” says Newshel. “But the new business wasn’t profitable business.” The poor business conditions are why many of the major insurers, such as UnitedHealth and Aetna to name a few, have pulled out of the exchanges in many states already and others are considering it.

Centene’s fortunes could dim under the new Republican plan, says Kim Monk, managing director at Capital Alpha Partners. The reason: the GOP’s new American Health Care Act will in 2020 begin scaling back sizable government subsidies that low-income Americans relied on to make coverage affordable. In the place of subsidies would be tax credits — based on age and income. Credits would range from $2,000 for people under 30 to $4,000 for those over 60, and be phased out for individuals earning more than $75,000 and $150,000 for couples that file joint tax returns. The problem is these tax credits won’t cover as much of the premium cost as the ACA, when the government footed nearly the entire bill. The result will likely be less people insured under Medicaid.

“It is a big risk for Centene if they lose a big chunk of that business,” says Monk.

The new plan’s elimination of the mandate for people to get coverage or pay a penalty, coupled with a reduction in the Medicaid pool that will be able to afford coverage, means more Americans will go without insurance again. Analysts say it is hard to estimate how many people will lose coverage under the new plan, but the number is seen in the millions, they say.

"All in all, it means less individuals insured by the insurance market," says Vishnu Lekraj, senior health care analyst at Morningstar.

The hit to most insurers' earnings might not be severe since many insurers have already exited the part of the ACA plan that involved the unprofitable exchanges, says Newshel. Bigger, more diversified insurers like UnitedHealth with smaller exposure to the individual coverage market will likely see a smaller impact on their overall earnings stream, Newshel says. If a new plan helps insurers strike the right balance between healthy people and sick people purchasing plans, profits in the market for individual market could improve.

Other factors offsetting some of the lost revenue if more people opt out of coverage are the new parts of the proposed plan that allow insurers to increase premiums by 30% for people who seek out insurance after a gap in coverage. In addition, starting in 2019, insurers will be able to charge higher premiums to older people. Under the new plan, insurers can charge older people five times what they charge younger ones. Under the ACA the ratio was 3 to 1.

“That’s all pretty positive for insurers,” says Monk of Capital Alpha.